The Rise of the Neo-Integrator

In a typical industrial robot deployment, hardware accounts for 40-50% of the total cost. The rest is engineering services related to deployment costs billed by a Systems Integrator.

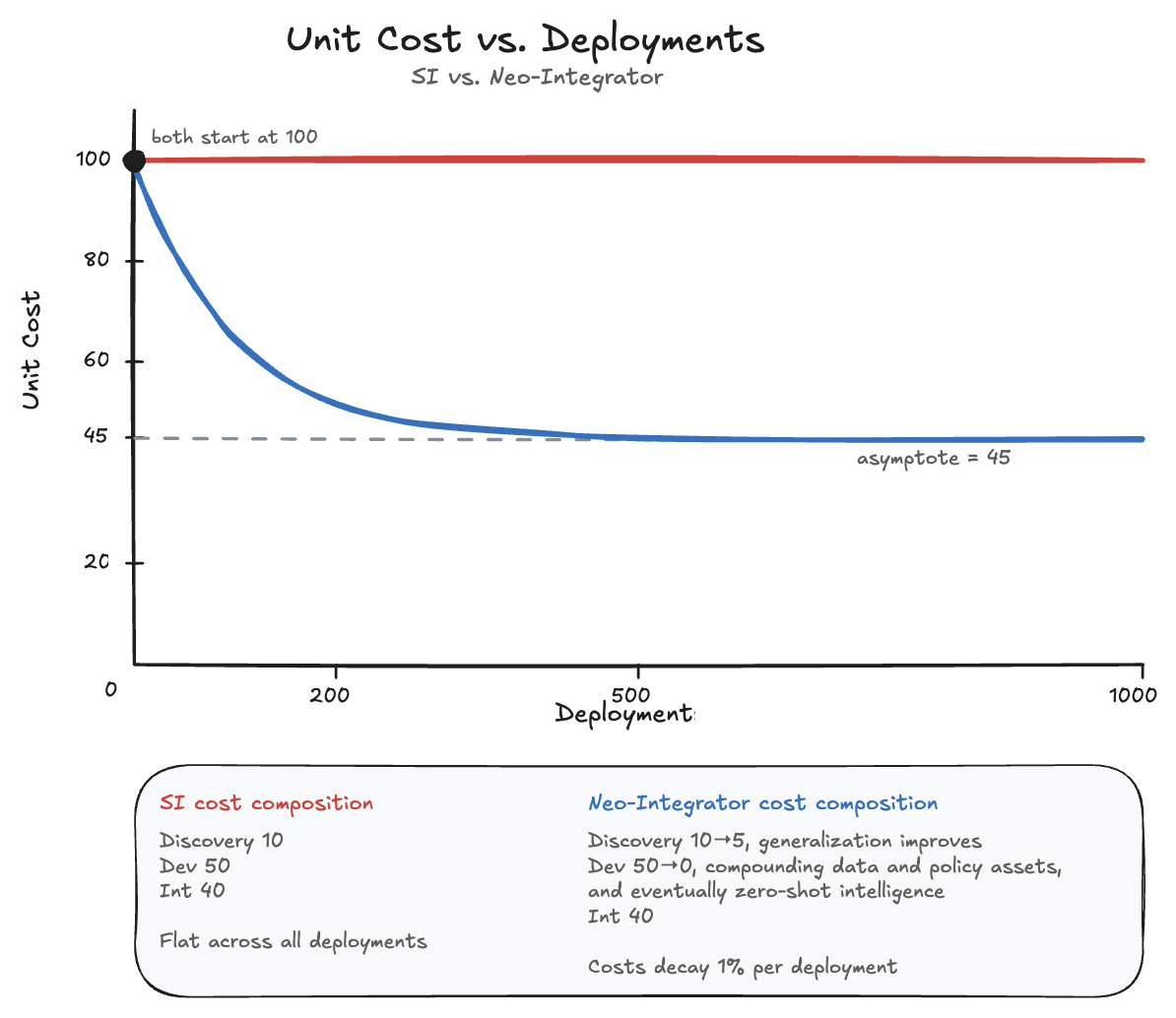

SIs are the forward-deployed engineers of robotics and are responsible for 70% of the ~400k industrial robots deployed in the US today. Their work breaks into three phases: discovery (what to automate and where), development (designing the cell, writing robot paths, configuring vision, handling edge cases), and integration (mounting, networking, safety review, WMS/MES/PLC integration, operator training, debugging, maintenance). Today, development and integration dominate every project budget. They’re also where SIs earn their margins on billable hours, which creates a perverse incentive: SIs make money by spending more time on each project, not less.

There are three structural reasons SIs charge what they charge:

The labor is scarce. Demand for industrial automation engineers is growing 10%+ annually; supply is growing 1-2%. Trade school enrollment isn’t closing the gap, and the senior engineers who provide deployment oversight are starting to retire.

Deployment is a one-time cost for the customer. Most customers automate intermittently, so they hire contractors instead of full-time staff. Contractors charge a premium in every industry.

SI margins come from billable hours. That rewards engineering time, not throughput, and creates a structural force against faster or cheaper deployment.

The composite effect is a cost floor that excludes most physical work. Automation is economical only for tasks with enough volume and margin to amortize a six- or seven-figure deployment, which is why industrial automation, after fifty years, is still concentrated in auto manufacturing, electronics assembly, and a handful of other high-throughput verticals. The same structure makes industrial cells effectively non-repurposable: changing the task usually means re-engineering the cell.

Robot learning is changing this — or so we hope. Recent robot foundation models are starting to show capabilities that once seemed impossible, and by turning bespoke development into reusable data and policies, they compress a meaningful share of deployment cost. But they don’t compress all of it. The physical work of integration stays mostly intact. This gap between what models can do in a lab and what it takes to make them work on-site is usually framed as capability vs deployability. The framing is fine for engineers but fails to illustrate where the business opportunity is.

Two questions structure the rest of this piece: where does robot learning actually reduce deployment cost, and which layer captures the surplus?

The Neo-Integrator Playbook

The old development cycle for deployments was largely custom engineering: a technician writes the robot’s paths, tunes the vision system, handles edge cases. The new development cycle is teleoperation, data collection and processing, and model post-training. The labor mix shifts from scarce SI technicians and engineers get replaced by two cheaper, more available inputs: teleoperators who collect data and run supervised deployments, and ML engineers who own the policy lifecycle. In a foundation model regime, data and policy assets carry forward. Though their value is bounded by overlaps in embodiments, tasks, and environments, the marginal cost of development falls with each deployment.

Discovery and integration look mostly the same. Discovery begins to benefit from repurposeability of a robot as generalization of models becomes a reliable feature (e.g. cross-embodiment). Integration is still site-specific and labor-intensive: safety reviews, mounting, networking, WMS/PLC/MES integration, operator training, exception handling, maintenance, etc. As development cost compresses, integration becomes the larger share of total cost, which may lead to more resource allocation to solve integration scalability.

These companies are “Neo-Integrators”. They use robot learning to reduce development. They use teleoperation to generate immediate revenue and training data. They own the customer relationship in a specific vertical. There are dozens of them already operating.

The Neo-Integrator playbook tracks the capability curve of the underlying models in three stages.

Stage 1: Teleoperation as a bridge. A teleoperated hour produces two things at once — revenue from a customer and post-training data for a model. Teleoperation isn’t a new technology but the economics around it are. Customers will pay for it because the alternative is staffing roles that are injury-prone, high-turnover, and hard to fill. Operators run cheaper than on-site labor because the work can be done remotely across geographies, within latency tolerances.

Stage 2: Autonomy expands margins. The end-state of robot automation may look more like Waymo’s human-in-the-loop than coding agents with a hybrid control stack of teleop, interventions, and sub-task automation, scaling gross margins without requiring end-to-end autonomy. Once enough teleoperation data is collected, autonomy takes over the steady-state tasks. The success rate of post-training regularly hits 95%+ in the lab (GEN-1, pi0.7), though production deployments of robot foundation models are still scarce.

The Neo-Integrator gets priority access to frontier models and post-training infrastructure. The Lab gets a real-world data pipeline funded by customer revenue, which is a more durable source of data than the standalone data vendors, and over time it may crowd them out.

Stage 3: Preparing for zero-shot. The North Star for Intelligence Labs is zero-shot intelligence. The North Star for Neo-Integrators is zero-shot deployment. A customer orders a robot, unboxes it, and gets value out of it the same day. The marginal cost collapses to shipping. Getting there requires solving problems that have nothing to do with model quality: hardware reliability, plug-and-play setup, fleet management, servicing and logistics, human-robot interfaces. Humanoid companies like Figure and 1X are betting they can achieve this on day one.

Why Neo-Integrators Will Win

The analogy to LLMs is useful but worth getting right. In LLMs, distribution is the API and the consumer brand, both of which are easily switchable. Anthropic and OpenAI defend that distribution by building products around the model (Claude Code, ChatGPT consumer surfaces) that compound usage and brand. In robotics, the distribution for intelligence is the robot itself which doesn’t exist yet on most customer sites. Eventually, model generalization cross-embodiments may make switching costs negligible but inside that window, the company that owns the deployment owns the customer.

Vertical specialization is the mechanism for building market share of deployments. The data flywheel and the integration playbook are vertical-specific. For example, a Neo-Integrator in 3PL warehousing accumulates warehouse-specific data (tasks, environments) and operational integration know-how that compounds within the 3PL space but doesn’t translate to food processing. Each 3PL facility may serve multiple customers with different inventory rules, billing logic, SLAs, labeling requirements, WMS configurations.

Customer psychology reinforces specialization. The buyers are typically operating lower margin businesses (<30%), and prioritize reliability, timing, and predictable costs. Once a Neo-Integrator’s robots are integrated into core workflows, the risk and expense of switching to a different stack rarely justify the marginal gain.

Once a Neo-Integrator has fleet density inside a customer site, the natural next revenue layers are complementary services such as fleet servicing and predictable maintenance contracts, parts and consumables (e.g. end effectors, sensors), and eventually insurance against hardware failure or reliability. None of these require new model capability. Traditional SIs sell into this surface too, but they sell it as billable hours. Neo-Integrators can sell these add-ons as a managed service priced against the labor it replaced.

The natural counter-question to Neo-Integrators positioning is why an Intelligence Lab doesn’t just capture this layer directly. There are three structural reasons they probably won’t, at least at scale.

First, organizational fit. The talent that trains frontier models is fundamentally different from the operational muscle needed to deploy and maintain robots in customer facilities. Moving downstream means standing up sales, field operations, and high-touch customer support effectively creating a second company running alongside the first.

Second, platform cannibalization. A Lab competing with its own Neo-Integrator partners risks collapsing the ecosystem it’s building, granted ecosystems are still small and immature today. The per-unit margin in deployment is attractive, but it’s dwarfed by the multiplier of being the model layer for every Neo-Integrator in the market once generalization becomes a reality.

Third, revenue profile. Vertical integration means concentrated, lumpy revenue dependent on landing enterprise contracts. An infrastructure play means a smoother, diversified revenue base across many partners. The latter is a better fit for the capital intensity of frontier training runs, and the Labs are the most capital-intensive R&D operations in the world.

A Lab could in principle run a hybrid open ecosystem for most verticals, vertical integration in a few high-margin niches like surgical robotics. The base case is that Labs stay where they are and Neo-Integrators capture the deployment surplus on top.

Conclusion

The economic prize in robotics is a system for making deployment repeatable. That system is what the Neo-Integrator is building — part integrator, part data company, part vertical software, part hardware OEM. Arguably, one of those layers isn’t defensible on its own today but owning all of them, inside a vertical is.

For founders, the implication is straightforward. Start a Neo-Integrator in a vertical with weak labor economics and enough task overlap that the data compounds. The model layer will commoditize toward a handful of Labs, and with the right partnerships, your company will ride that wave.